[ad_1]

In the Altos Research data, we track every home for sale in the country every week. We can see the momentum of these changes immediately.

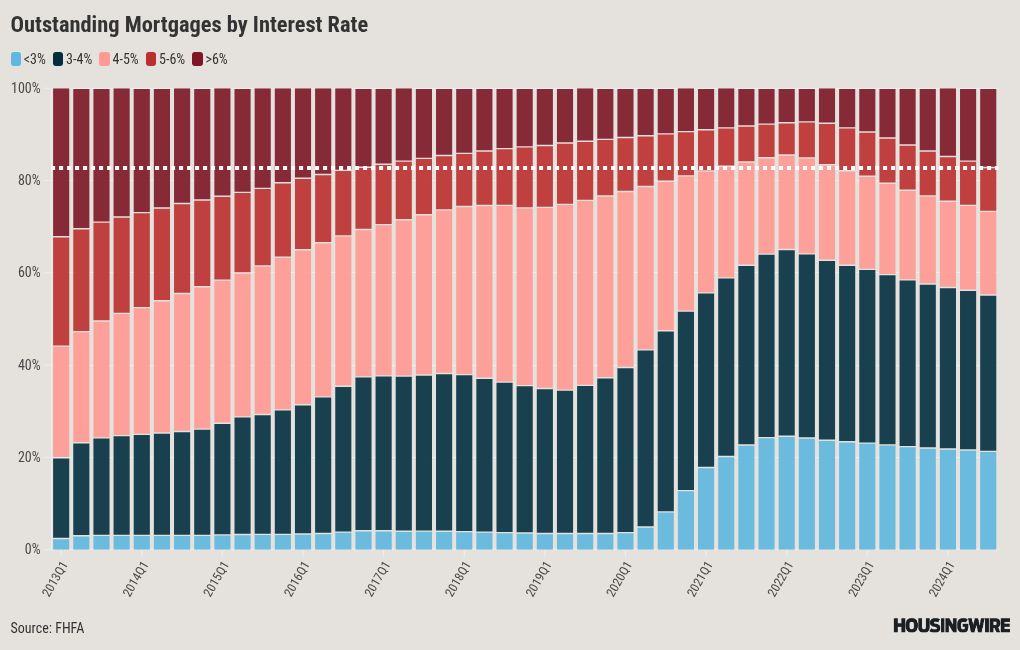

We can see this impact in any number of statistics. Tenure of ownership keeps climbing. We used to hold homes for seven years — now we hold them for about 10 years. The average age of outstanding loans climbed steadily during the cheap-money decade, dropped during the pandemic frenzy and is now skyrocketing as homeowners hunker down. The average age of all outstanding mortgages is now 72 months, up from just 59 months at the end of the pandemic free-money boom.

Cheap mortgage rates, locked in for 30 years, make people want to hold on to their homes. The opposite is true too: As mortgages get more expensive, more homeowners want to sell their homes.

People with expensive mortgages are more likely to sell their house. They’ll sell when it’s their primary residence — to finance the next home. They’ll sell investment properties — where the cash flow just doesn’t pencil like it would with a 4% loan. They’ll unload some of the properties with ultra-cheap loans to finance the next purchase. The more folks with expensive loans, the greater the available inventory of homes on the market.

By June this year, we should expect that over 20% of U.S. borrowers will have mortgages with a 30-year fixed rate greater than 6% — levels not seen for a decade. As long as mortgage rates stay elevated, which seems likely for at least 2025, we’ll build a market with more and more homeowners with expensive mortgages.

The impact will be felt for years.

The next 5 years

We could end the year with more than 10 million homeowners with these expensive mortgages. Compare this to just over 3 million as we emerged from the pandemic frenzy in Q1 2022. That’s a lot more would-be home sellers when the time comes. Not all of them are ready to sell right now, of course. Life events take time to materialize. But each year with higher rates means more willing home sellers.

In 2025, we expect unsold inventory of homes on the market to get very close to the 2018 levels. If mortgage rates stay elevated into 2026, we could easily see inventory grow back to 1 million homes or more — levels that we used to consider normal a decade ago.

What happens when we have all these homes on the market? More selection for buyers, for one thing. In the last 10 years, homebuyers, especially first-time homebuyers, have been trapped in competitive situations, with poor selection and often bidding wars. Only the best-prepared buyers would win. In the next few years, this implies better opportunities for beleaguered homebuyers who have been battling for scraps of inventory since 2015. The pressure finally subsides.

There will be less upward pressure on home prices. Home prices have pressed relentlessly higher across the country — even when demand was low in 2023 and 2024, supply was still so tight in many markets that home prices rose. That trend is now flat for home prices for several more years, maybe even to the end of the decade.

It also means muted equity increases. It’ll be a much more risky era to buy with a very low down payment. It’ll be an era where fewer investors can speculate by buying multiple properties with the equity gains of an existing portfolio.

As home prices stay flat for multiple years, it means incomes will increase faster than home price, so affordability improves over the rest of the decade. Stubbornly high mortgage rates as our path to finally solving the affordability crisis in America? Wouldn’t that be an ironic outcome?

[ad_2]

Source link